Can I Lose My 401(k) If the Market Crashes?

Market downturns can be unsettling, especially when your retirement savings are tied to the stock market. If you’ve ever checked your 401(k) balance during a period of volatility and wondered whether you could lose everything, you’re not alone. This is one of the most common concerns among retirement savers, particularly during economic uncertainty.

The good news is that while market crashes can reduce the value of your investments, they do not automatically mean your 401(k) will disappear. Understanding how 401(k) plans work, what happens during market downturns, and how to manage risk can help you make informed decisions and protect your long-term financial future.

What Is a 401(k) and How Does It Work?

A 401(k) is an employer-sponsored retirement savings plan that allows workers to invest a portion of their income for retirement. Contributions are typically invested in mutual funds, index funds, target-date funds, bonds, or other investment options offered within the plan.

The value of your 401(k) depends on the performance of the investments you select. When markets perform well, your account balance may grow significantly. When markets decline, your account balance may decrease.

However, it’s important to remember that a 401(k) is not a bank account. Its value fluctuates because it is invested in financial markets.

What Happens to Your 401(k) During a Market Crash?

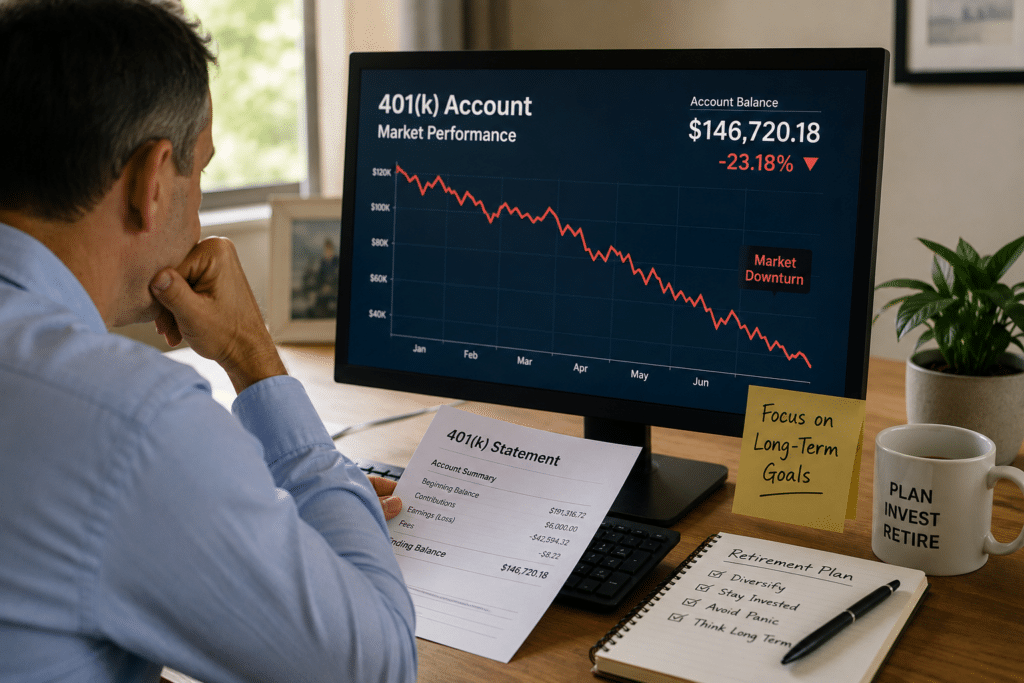

When the stock market crashes, the investments within your 401(k) may lose value temporarily.

For example:

- If your account balance is $200,000 and the market declines by 20%, your balance could fall to approximately $160,000.

- If the market recovers over time, your account may regain value.

- The actual impact depends on your investment allocation and risk profile.

Market downturns affect most retirement accounts because many retirement plans are heavily invested in stocks and equity-based funds.

The key word here is temporary.

A decline only becomes permanent if investments are sold while prices are down.

Can You Lose All Your Money in a 401(k)?

In most cases, the answer is no.

While severe losses are possible, it is extremely rare for a diversified 401(k) portfolio to go to zero.

For a retirement account to lose all value, every investment within it would essentially have to become worthless. Most 401(k) plans are diversified across numerous companies, industries, and asset classes, which significantly reduces this risk.

That said, investors can experience substantial losses during major economic downturns.

Examples include:

The Dot-Com Crash (2000–2002)

Many technology stocks lost significant value, causing retirement accounts heavily concentrated in tech investments to decline sharply.

The Financial Crisis (2008)

The S&P 500 fell more than 50% from its peak, leading many retirement accounts to experience substantial temporary losses.

The COVID-19 Market Decline (2020)

Markets dropped rapidly before recovering and eventually reaching new highs.

These examples show that while retirement accounts can lose value during market crashes, markets have historically recovered over time.

Why Many Investors Lose More Than Necessary

One of the biggest risks during a market crash is not the crash itself—it’s emotional decision-making.

When markets decline sharply, some investors panic and sell their investments to avoid further losses.

Unfortunately, this often locks in losses and prevents participation in future recoveries.

Consider two investors:

Investor A

- Keeps investments during the downturn

- Continues contributing

- Participates in market recovery

Investor B

- Sells during the crash

- Moves entirely to cash

- Misses the recovery period

Historically, Investor A often ends up with better long-term results.

This is why financial professionals frequently emphasize maintaining a long-term perspective.

Factors That Determine How Much Your 401(k) May Lose

Not every retirement account experiences the same level of decline.

Several factors influence how a market crash affects your savings.

Asset Allocation

Accounts invested primarily in stocks generally experience larger swings than those holding a mix of stocks and bonds.

Age and Retirement Timeline

Investors nearing retirement may choose more conservative allocations to reduce exposure to market volatility.

Younger investors often have decades before retirement and may have more time to recover from downturns.

Diversification

Diversified portfolios typically perform more consistently than portfolios concentrated in a single sector or asset class.

Market Conditions

Every downturn is different. Economic factors, interest rates, inflation, and global events can all influence recovery timelines.

How to Protect Your 401(k) From a Market Crash

While no investment strategy can completely eliminate risk, several approaches may help reduce exposure to significant losses.

Diversify Your Portfolio

Diversification spreads investments across multiple asset classes rather than relying on a single market sector.

A diversified retirement portfolio may include:

- U.S. stocks

- International stocks

- Bonds

- Cash equivalents

- Alternative assets

Diversification can help reduce overall portfolio volatility.

Review Your Risk Tolerance

Your investment strategy should align with your goals, age, and comfort with market fluctuations.

An aggressive portfolio may offer higher growth potential but also greater volatility.

A more balanced allocation may provide additional stability during uncertain market conditions.

Continue Investing During Downturns

Many investors stop contributing when markets decline.

However, continuing contributions during downturns may allow investors to purchase assets at lower prices, potentially benefiting from future recoveries.

This strategy is commonly known as dollar-cost averaging.

Avoid Emotional Decisions

Market headlines often create fear during periods of volatility.

Having a long-term plan and sticking to it can help prevent costly mistakes driven by short-term emotions.

Can Diversification Beyond Traditional Assets Help?

Many investors explore additional ways to diversify retirement savings beyond traditional stock and bond investments.

Alternative assets may include:

- Precious metals

- Real estate

- Private investments

- Cryptocurrency

- Other self-directed retirement investments

The purpose of diversification is not necessarily to increase returns but to reduce reliance on a single asset class.

Precious metals remain one of the most popular alternative retirement investments because they have historically served as stores of value during periods of market uncertainty. Investors often consider a Gold IRA or Silver IRA when looking to diversify retirement savings beyond stocks and bonds.

The Potential Role of Precious Metals in Retirement Planning

Precious metals such as gold and silver have historically been viewed as stores of value during periods of economic uncertainty.

Some investors choose to allocate a portion of their retirement portfolio to precious metals through a Self-Directed Gold IRA or Silver IRA, allowing them to hold IRS-approved precious metals within a tax-advantaged retirement account.

Potential reasons include:

- Inflation concerns

- Currency uncertainty

- Market volatility

- Long-term wealth preservation

However, precious metals should generally be viewed as one component of a diversified retirement strategy rather than a complete replacement for traditional investments.

When Should You Consider a 401(k) Rollover?

A rollover may be worth exploring if:

- You have left an employer.

- You want more control over investment options.

- You are seeking broader diversification opportunities.

- You are evaluating alternative retirement investment strategies.

Before making any decisions, it is important to understand the rules, costs, and potential tax implications associated with retirement account rollovers.

Could a Gold IRA Help Protect Your Retirement Portfolio?

A market crash does not necessarily mean investors should abandon traditional investments. However, many retirement savers choose to diversify a portion of their portfolio with physical precious metals.

A Gold IRA allows investors to hold IRS-approved gold within a tax-advantaged retirement account, while a Silver IRA provides similar access to physical silver investments. These assets may offer diversification benefits and can help reduce reliance on stock market performance alone.

While market downturns can temporarily reduce the value of your retirement savings, a crash does not automatically mean your 401(k) is gone. Historically, diversified retirement portfolios have weathered market cycles and benefited from long-term recovery.

Frequently Asked Questions

Can a 401(k) go to zero during a market crash?

While a 401(k) can lose significant value during severe market declines, it is extremely uncommon for a diversified retirement account to lose all value.

Should I move my 401(k) to cash during a market crash?

Many financial professionals caution against panic selling because it can lock in losses and cause investors to miss potential recoveries.

How long does it take for a 401(k) to recover after a crash?

Recovery timelines vary depending on market conditions. Historically, major market downturns have eventually recovered, though recovery periods can range from months to several years.

Is diversification important for retirement investing?

Yes. Diversification helps reduce concentration risk and may improve portfolio stability over the long term.

Can alternative assets be held in retirement accounts?

Certain retirement account structures may allow access to alternative assets, depending on applicable rules and regulations.

While market downturns can temporarily reduce the value of your retirement savings, a crash does not automatically mean your 401(k) is gone. Historically, diversified retirement portfolios have weathered market cycles and benefited from long-term recovery.